Budgeting can often feel overwhelming, but it doesn’t have to be. Using pen and paper for budgeting enhances financial awareness and encourages mindfulness in spending habits. This practical approach allows individuals to engage actively with their finances, making them more accountable for their choices.

Combining traditional journaling techniques with modern financial tracking allows one to create an effective personalized system. Writing things down helps clarify thoughts and organize expenses, leading to better financial management.

Many find that this tactile method facilitates a deeper connection to their financial goals, making budgeting less of a chore and more of an empowering activity. With the right tools and mindset, anyone can transform their financial journey through effective journaling practices.

Budget journaling offers a structured approach to financial awareness. It enables individuals to understand their spending habits and make informed decisions by bridging emotional and rational aspects of financial management.

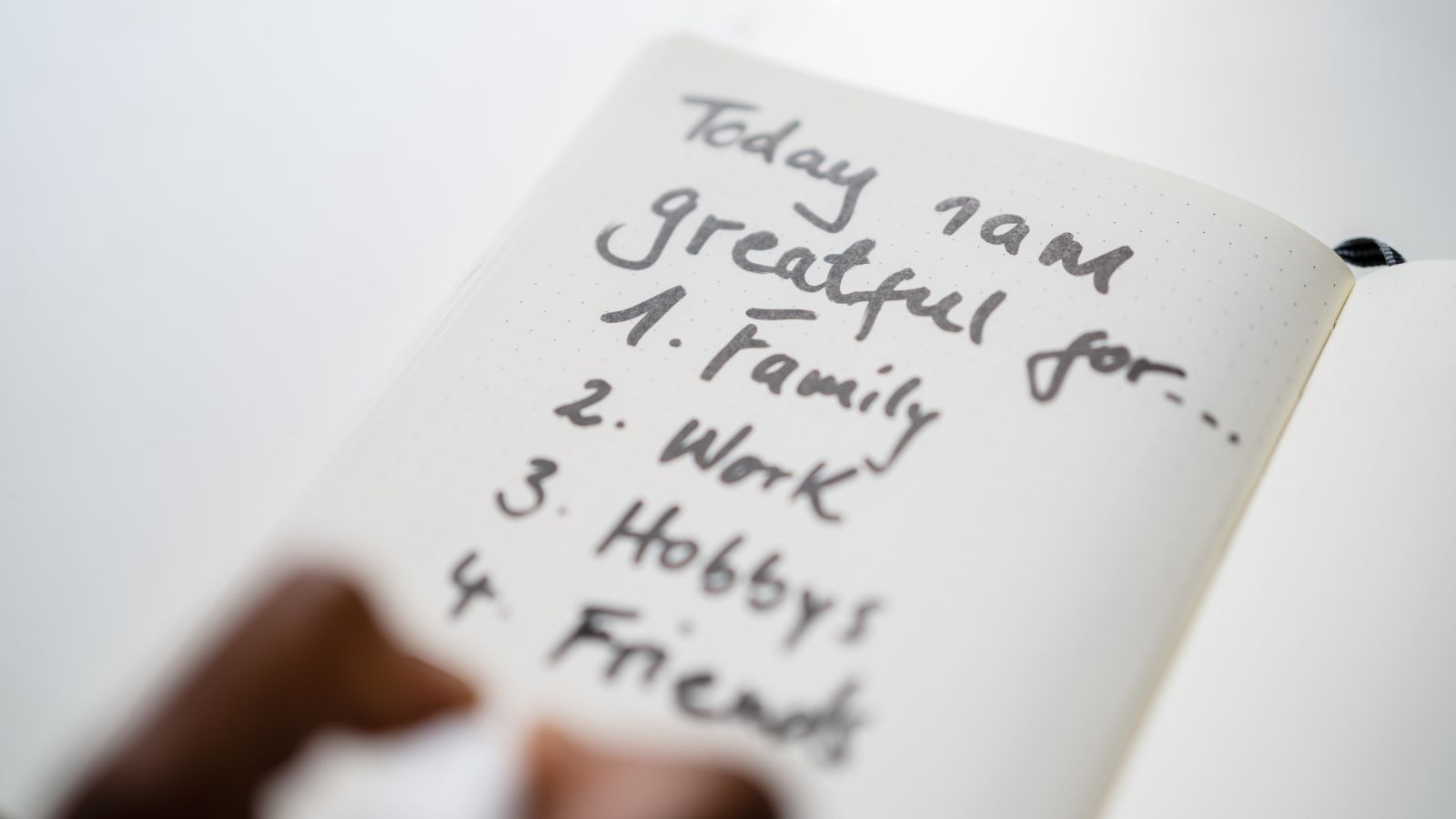

Every person has a unique financial story that shapes their behavior. Budget journaling provides a platform for individuals to document their income, expenses, and saving goals. This practice helps reveal patterns in spending, enabling deeper insights into their financial choices.

By recording every transaction, he or she can identify areas of overspending or opportunities for saving. This reflective practice promotes accountability, as writing down expenses often brings awareness and clarity.

Using prompts and reflective questions can further enhance this narrative. Journals can include sections for setting financial goals alongside a monthly summary of expenses, making it easier to track progress.

Behavioral finance examines the psychological factors that influence financial decisions. Budget journaling is a practical tool for incorporating this discipline into daily life.

Recording financial activities helps individuals confront biases and emotional triggers. Understanding impulse purchases or emotional spending can lead to better decision-making.

Incorporating techniques from behavioral finance, such as setting aside time for reflection, can deepen one’s understanding of spending habits. Budget journals also allow for goal-setting, promoting positive financial behavior through consistent tracking.

By melding behavioral finance principles with journaling, individuals can create a feedback loop that reinforces mindful spending and better budgeting practices.

Establishing a budget journal involves selecting the right materials and tools that will contribute to effective financial tracking. Attention to detail in this setup phase can enhance the budgeting experience.

Selecting an appropriate journal is crucial for creating a budget that is both functional and enjoyable to use. A durable notebook with enough space is ideal. Consider options like:

Size matters, too. A portable journal is helpful for budgeting on the go, while a larger one can suit at-home planning. Finally, choose a cover design that inspires and motivates ongoing use.

In addition to the journal, some essential tools can enhance the budgeting process. The following items are recommended:

Combine these tools with regular reviews of entries. Consistency in documenting finances reinforces tracking habits and reveals spending trends. These elements work together to create a comprehensive and engaging budgeting process.

Creating a comprehensive budget plan involves careful attention to various key aspects. A clear structure helps ensure that all financial areas are addressed efficiently.

Accurate income tracking is essential for effective budgeting. Begin by documenting all sources of income, such as salaries, bonuses, freelance work, and passive income. This can be done using a simple table:

| Source of Income | Amount |

| Salary | $3,000 |

| Freelance Work | $500 |

| Investments | $200 |

| Total Income | $3,700 |

Consider using both monthly and annual perspectives. Noting different sources helps in understanding total earnings and planning expenses accordingly. Regular updates will ensure the budget reflects current income.

Categorizing expenses is vital for budget clarity. Break down spending into essential categories such as housing, utilities, groceries, transportation, entertainment, and savings. An example categorization might look like this:

Reviewing these categories monthly helps identify spending patterns and areas for potential cuts. This targeted approach allows for better management of discretionary funds while still meeting essential needs.

Allocating funds for savings and investments is crucial to building financial security. A structured approach includes setting aside a specific percentage of income. Common guidelines suggest:

A breakdown of this allocation ensures funds are directed towards both short-term and long-term goals. Using a budgeting app or spreadsheet can help track these allocations effectively. Regular contributions to savings and investment accounts foster financial growth over time.

Analyzing expenses thoroughly allows individuals to identify spending patterns and make informed financial decisions. Understanding the distinction between fixed and variable expenses is crucial, as well as recognizing opportunities to reduce unnecessary costs.

Fixed expenses are consistent monthly costs that typically do not fluctuate. Common examples include rent or mortgage payments, insurance premiums, and subscription services. Individuals can rely on these expenses for budgeting because they remain the same each month.

In contrast, variable expenses change based on usage or lifestyle choices. Groceries, dining out, entertainment, and utility bills fall into this category. Tracking these expenses closely can reveal significant savings opportunities. For effective budgeting, a person should categorize expenses into fixed and variable groups to better understand where their money is going.

Identifying unnecessary costs involves scrutinizing discretionary spending. This includes evaluating subscriptions, memberships, and habitual purchases. Creating a list can help visualize where money goes each month.

To cut costs effectively, one can consider canceling unused subscriptions or negotiating bills with service providers. Implementing a 30-day rule before making non-essential purchases may aid in reducing impulse spending. Tracking variable expenses can also highlight patterns that suggest areas for potential savings. By being mindful of spending, individuals can make informed decisions that align with their financial goals.

Incorporating specific journaling techniques can provide essential insights into one’s financial situation. Regular reflections and goal visualization enhance budgeting effectiveness and decision-making.

Setting a schedule for regular financial check-ins fosters accountability. This practice involves reviewing expenses, income, and savings at specified intervals, such as weekly or monthly.

During check-ins, individuals can document any variances from the budget. Noting unexpected expenses or income helps identify patterns over time. Utilizing a simple table can aid in summarizing financial status, tracking goals, and highlighting areas needing adjustment.

An effective approach can include categories like Income, Fixed Expenses, Variable Expenses, and Savings Goals. This structure aids clarity and facilitates informed decisions moving forward.

Visualization strengthens commitment to financial objectives. Creating a vision board or using journaling prompts directs focus on specific goals, such as saving for a vacation or paying off debt.

A useful technique is to write detailed descriptions of these goals. Include numbers, timelines, and feelings associated with achieving them.

Incorporating drawings or charts can also enhance motivation. For instance, a simple bar graph showing progress toward a savings goal can be both encouraging and informative.

This visual approach makes targets tangible and reinforces the importance of budgeting. It serves as a constant reminder of what one strives for, encouraging disciplined financial behavior.

Life changes can significantly impact financial situations. Therefore, adapting a budget journal to reflect these changes is essential for effective money management.

Common Life Changes:

Adjusting Your Journal:

Implementation of these adaptations will streamline the budgeting process. A flexible approach will allow the budget journal to remain a practical tool for financial management through various life transitions.

Monitoring progress is essential in any budgeting process. Regular reviews of income and expenses help identify trends and areas for improvement.

Steps to Monitor Progress:

| Category | Budgeted Amount | Actual Amount | Difference |

| Food | $300 | $320 | -$20 |

| Utilities | $150 | $140 | +$10 |

Using Journals for Tracking:

A journal can be an effective tool. It allows for not only tracking but reflecting on spending habits:

By consistently monitoring and adjusting, one can achieve greater financial control and improvement.

Regular reflection on financial habits can provide valuable insights. By evaluating past experiences, individuals can identify patterns and achieve better budgeting outcomes.

Conducting reviews every six months allows individuals to assess their spending and saving habits comprehensively. During these reviews, it’s essential to examine income changes, unexpected expenses, and progress toward financial goals.

Creating a simple table can assist in this analysis. For example:

| Category | Budgeted Amount | Actual Amount | Difference |

| Groceries | $300 | $350 | -$50 |

| Entertainment | $100 | $80 | +$20 |

This format highlights areas that may need adjustment. Adjusting budgets in response to real spending can lead to more accurate planning for future periods.

Reviewing past entries in a budgeting journal can reveal significant trends and behaviors. By noting recurring expenses that exceed budgeted amounts, individuals can identify the triggers behind overspending.

For instance, consistent overspending on dining out might indicate a need for better meal planning.

Additionally, journaling can highlight successful strategies as well. Recognizing periods of savings success can motivate continued positive behaviors.

By categorizing experiences, individuals can better understand their financial journey and refine their approach moving forward. Each entry serves as a reflection point for smart financial decisions.

Stay Updated with the Latest Reviews – Subscribe to Our Newsletter!

As an Amazon Associate, Journaltreats.com earns from qualifying purchases.

Our website also contains other affiliate links, but our editorial content is not influenced by advertisers or affiliate partnerships. See our full disclosure.

AI Disclosure: Some elements may have been created with the assistance of AI tools.

All of the content on this website, including images, text, audio, and video, is Copyright © 2024 Journal Treats and may not be stolen, reproduced, downloaded, republished, or otherwise used without the explicit written permission of the owner of Journaltreats.com.

Except where prior permission is granted, Journal Treats reserves all rights.